CosmicTaco

General Catalyst's Venture Highway Acquisition: A Strategic Play for India 🇮🇳

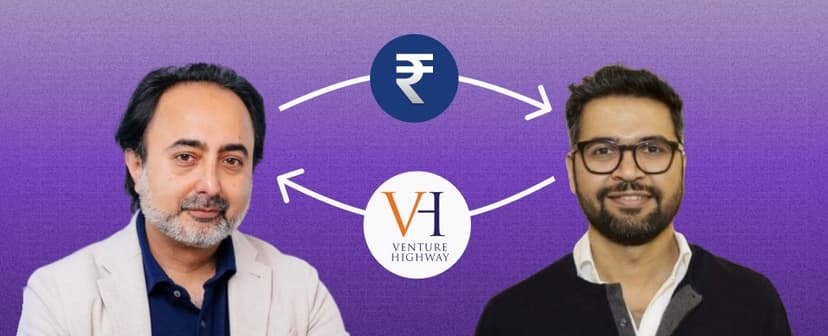

In a landmark deal, Silicon Valley powerhouse General Catalyst has acquired Venture Highway, a seed-stage investment firm with a track record of backing winners like Meesho and Mobile Premier League.

The Deal:

- Rare instance of consolidation in the Indian VC market

- VH to be rebranded as General Catalyst India

- GC plans to invest $500 million to $1 billion in India over the next three years

- Acquisition driven by desire to build strong local team and tap into local LP network

But the move also raises important questions. Will this trigger a wave of consolidation in the Indian VC market? Will other global firms follow suit and snap up local players to gain a foothold in the country? And how will this influx of foreign capital shape the trajectory of India's startup ecosystem?

As the dust settles on this landmark deal, one thing is clear: India's startup scene is entering a new era, one where local innovation and global capital are increasingly intertwined. Always long on India 🇮🇳

Image Credits: The Arc

7mo ago

Find out if you are being paid fairly.Download Grapevine

Discover more

Curated from across