Personal Finance18mo

by PerkyNuggetKotak Mahindra Group

Is Stable money a stable choice ?

I personally see it as game changer in how invest in FDs.

Any comments or thoughts or guidance would be highly appreciated.

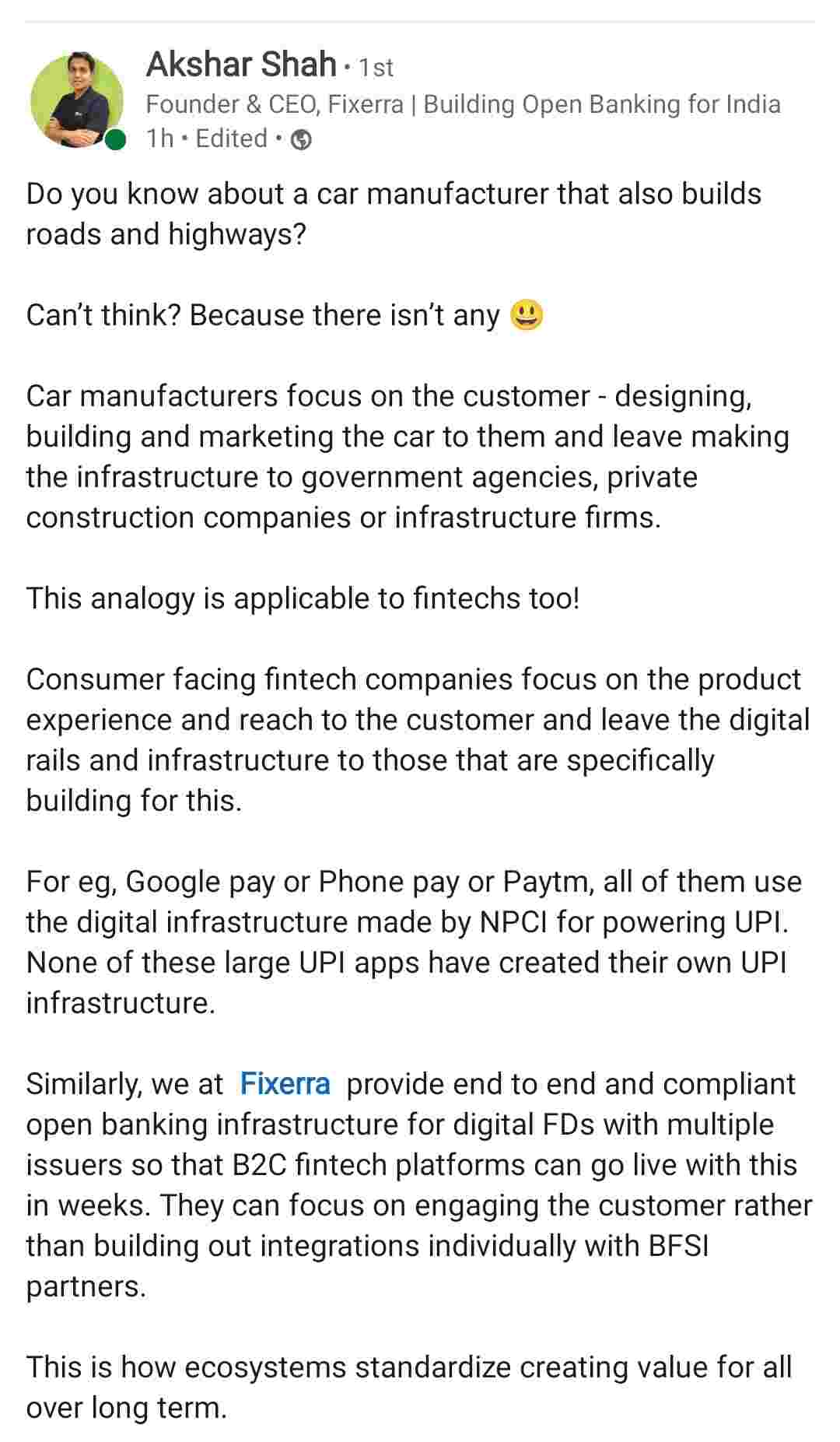

Does this affect the stable money value prop.? Because as mentioned in the post fixerra is bringing in multiple FD issuers and providing infrastructure to build. Would that lower the entry barrier for building B2C product in FD segment as any fintech can expand horizontally in this segment by integrating with them.

Or stable money themselves are using these types of tools as an enabler? Just wanted to understand if I'm thinking this right?

Stable money is a financial product distributor. So the only way they can get ahead is showing large number of investors and AUM. Financial product distributors won’t have a strong moat. It’s about who has the most VC money to acquire users. And the margins for distribution of FD is max 1%. So they won’t even make money even if they achieve a large AUM. So they will eventually start lending

Customers money will be with AUM not with Stable money and with thin margin of 1% how will they start lending and how can a savings platform start lending on their platform it's like a store selling both Nicotine gum and cigarettes

And worth mentioning India's BNPL poster child Zest money huge failure

I believe fintech is all about transparency and giving power back to people that's what banks failed to do but now banks have also realised it's not just the infra they have to provide a good user experience like HDFC sky

@Soprano90 yup makes sense. Agreed on the thin margins and no strong moat part. But somewhat lending doesn't make sense for them in the short term as @Gonxkillua mentioned but might be an option in a long term vision.

But @Gonxkillua then how will they achieve profitability or make a significant chunk of profit. Because even after achieving scale, 1% margin business is not worth pursuing.

Maybe in that case they somehow pivot to lending for a particular segment once they have enough user base and loyal customers. Because even startups like Refyne started with an earned wage access model is looking to be a NBFC for a particular segment (blue collar workers).

Multiple players exist in digital FD market, for example - M2P

https://m2pfintech.com/blog/how-can-banks-and-nbfcs-leverage-the-potential-of-digital-fds/

I personally see it as game changer in how invest in FDs.

Any comments or thoughts or guidance would be highly appreciated.

Hey GVers !

Not sure how many of you have noticed but Stable money UX changes drastically whenever you click on Invest in a FD, this made me think why their design language is so different in 2 screens, upon further research, I figured ...

So stable money is just another fintech platform where basically you can do FD from various banks and corporates.

This concept isn't new, other apps and websites offer the same as well.

Weirdly, everyone is posting about it on LinkedIn...

Hi Grapevine,

I'm Saurabh, currently building Stable Money, India’s largest platform for fixed return investments.

I'd love to chat with you folks about my ...

Hi Saurabh, Thanks for doing this. As somebody in their 20s who invests in mutual funds and stocks primarily, wh...